Legal | Tax | Compliance

Legal | Tax | Compliance

With the acceptance of the Tax Reform and AHV Financing ("TRAF") by the Swiss voters, various tax incentives were introduced in the Federal Act on the Harmonisation of Direct Taxes (FTHA). Among others, the cantons can allow an additional deduction for research and development carried out in Switzerland ("R&D super-deduction").

According to Art. 25a para. 1 FTHA, the cantons may allow an additional R&D deduction of up to 50% on the business-related research and development expenses. Due to the wording "the cantons may" as well as "up to 50%", it is up to the cantons whether they (i) allow the R&D super-deduction in general and (ii) to what extent it will be allowed (within the limit set by the FTHA). The following link contains an overview of the availability and the respective percentage of an additional R&D deduction in the cantons.

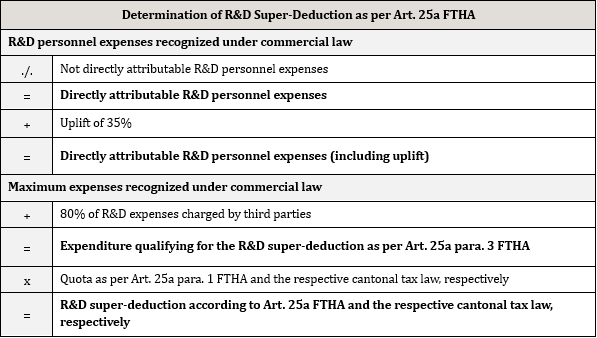

According to Art. 25a para. 3 lit. a FTHA, the additional R&D deduction is granted on the personnel expenses directly attributable to research and development recognized under commercial law, plus a surcharge of 35% on these personnel expenses ("uplift"). However, the personnel expenses directly attributable to research and development plus the uplift must not exceed the total expenses recognized under commercial law. In addition to a company’s own R&D personnel expenses, a deduction of 80% of the expenses for research and development invoiced by third parties is permitted. If a company is engaged as a service provider in an R&D project, Art. 25a para. 4 FTHA assigns the right of the R&D super-deduction to the service recipient. As a result, in general, the service recipient is entitled to the R&D super-deduction. However, if the service recipient is not able to use the R&D super-deduction (e.g., the respective cantone has not implemented the R&D super deduction in its cantonal tax law), the service provider can claim for the R&D super-deduction.

The amount of the R&D super-deduction is to be determined as follows:

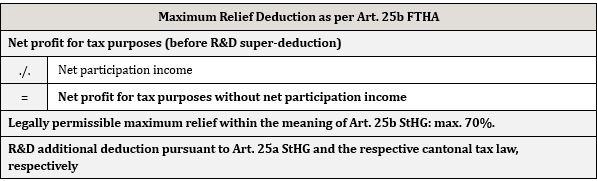

Maximum Relief Deduction

Art. 25b FTHA limits the overall tax relief - disregarding the net participation income - to a maximum of 70% of the taxable profit before offsetting losses. The amount of the maximum relief deduction can be determined by the cantons themselves within the limit set by Art. 25b FTHA. As a result, the actual relief deduction in the cantons ranges from 9% to 70%. The following link contains an overview of the maximum relief deduction in the cantons.

The following table show the calculation of the R&D super-deduction, taking into account the maximum relief deduction:

Of the tax reductions introduced by the TRAF, the R&D additional deduction is internationally the most accepted instrument. In the European Union, in particular, the promotion of innovation has been proclaimed as one of the key elements for increasing competitiveness since the Lisbon Strategy was adopted in 2000. In this context, R&D promotion takes place, analogous to the Swiss model, via a super-deduction or alternatively via a so-called grant system.