Legal | Tax | Compliance

Legal | Tax | Compliance

Tokenization of investment funds offers efficiency, cost reduction, compliance improvements, liquidity, transparency, and innovation, but faces legal, technological, and market challenges.

When it comes to asset tokenization, it is essential to choose a blockchain that allows applications to be built directly on the blockchain. These applications are software programs known as smart contracts, which may serve almost any purpose. Given these two distinct but connected layers, it is important to distinguish between the protocol layer and the application layer.

The protocol layer refers to the blockchain as the underlying infrastructure. Article 973d of the Swiss Code of Obligations (“CO”) designates this layer (including further layers, cf. 2.2 below) as a «securities ledger», which is appropriate as blockchain is one type of distributed ledger technology (“DLT”). Blockchain can be described as a decentralized and cryptographically secured database in a peer-to-peer network. A blockchain can only be extended chronologically, for which consensus among the nodes is required. Due to these features, a blockchain is considered immutable.

Furthermore, nowadays, scalability solutions are now being built on top of most blockchains with the aim of making transactions faster, cheaper and more efficient. Strictly speaking, these scalability solutions form a separate layer as smart contracts (incl. DApps) can be built on top of such or be connected to such solutions. However, for the sake of simplicity of this short overview, such scalability solutions will not be further explained herein.

The application layer refers to smart contracts. Depending on its purpose, a smart contract might mint tokens which could reflect the value of an asset, entitle the token holder to a membership right or use, or represent ownership of an item. Depending on the use case and, in particular, for the tokenization of financial instruments in Switzerland, an in-depth examination of the financial market regulations and art. 973d et seq. CO must be performed prior to processing with the tokenization of real assets. Failure to comply with financial market regulations can have severe consequences and may result in high fines and a forced liquidation of the company.

In simplified terms, tokenization can be described as the process of digitizing an asset by creating a blockchain-based token. Combining this description with the Federal Department of Finance’s (“FDF”) understanding, tokenization can be defined as the creation of a digital representation of a digital or non-digital asset that is electronically registered and therefore tradable on the blockchain. Consequently, this digital representation of a digital or non-digital asset constitutes a token.

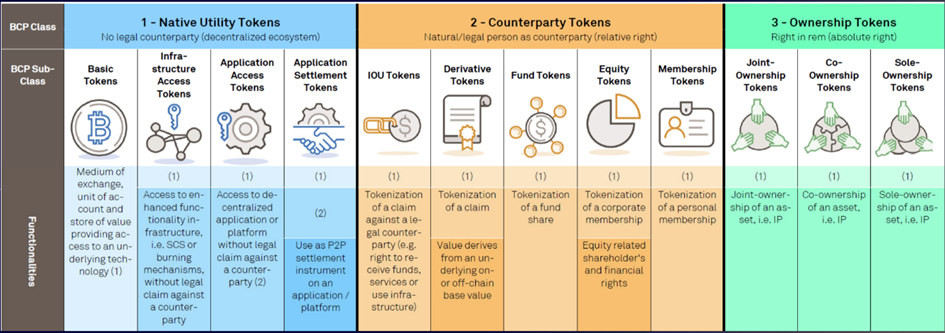

With this in mind, it would be reasonable to conclude that a token can be defined as a representation or linkage of a digital or non-digital asset. However, and with view to the BCP-Framework, which was introduced by MME in 2018[1] and is shown below, this is only true for so-called «Asset Tokens», «Counterparty Tokens», or «Ownership Tokens».

The categories of «Asset Tokens», «Counterparty Tokens», or «Ownership Tokens». truly represent a non-digital asset, e.g., a relative right or an absolute right to an asset. Accordingly, the represented right can only be transferred if the token is transferred, as the respective right and the token are inseparably interlinked as further explained below.

However, in this regard it must be noted, that the Swiss Financial Market Supervisory Authority (“FINMA”) does not distinguish «Asset Tokens» into further categories (cf. paragraph below).

In addition to the financial market regulations, which primarily aim to protect investors, in Switzerland, the Collective Investment Schemes Act (“CISA”) is the authoritative law when launching a Swiss-based investment fund. It might therefore be surprising that the CISA is irrelevant for the tokenization process of investment funds units. Hence, neither the fund structure nor its method of distribution (e.g., listed funds) are relevant for the tokenization of the investment fund unit. However – and make no mistake - the CISA applies to all Swiss-based investment funds regardless of whether their units are tokenized or not. For the legal qualification of a tokenized investment fund unit, however, other laws are relevant which is why some compare tokenization to securitization.

Tokenization and securitization may be compared to the extent that all claims (relative rights) can be securitized and therefore also tokenized in the sense of a “digital securitization”. Nonetheless, securitization refers to the representation of a relative right in either negotiable securities (Wertpapiere) or an entry in a centrally kept register and hence in uncertificated securities (einfache Wertrechte) or in intermediated securities (Bucheffekten). In case of corporate membership rights, however, securitization is only possible where the law permits it, i.e., in case of companies limited by shares (Aktiengesellschaft) and partnerships limited by shares (Kommanditaktiengesellschaft).

Conversely, tokenization goes further than securitization in the sense that not only securitizable rights/claims can be tokenized, but also non-securitizable rights, such as absolute rights or other membership rights, including investment funds units. Furthermore, tokenizing an asset aims to result in a ledger-based security (Registerwertrecht) and hence in a right that is electronically registered on a decentralized ledger – the blockchain.

From a private law perspective, tokenized shares or investment fund units generally qualify as ledger-based securities, provided the securities ledger (the blockchain including its respective layer [scalability solution and smart contract]) meets the requirements of art. 973d para. 2 CO. The category of ledger-based securities was specifically created in 2021 to recognize tokenized assets within Switzerland’s legal framework.

However, contrary to the term “ledger-based security”, not every tokenized share or investment fund unit automatically qualifies as a security in the sense of financial market law. For a tokenized share or unit to constitute a security under securities law, the following must be met cumulatively:

(i) the tokenized right must be transferable only through the token (securitization);

(ii) the token must be publicly offered in the same structure and denomination (standardization); and

(iii) the tokens must be fungible among each other (fungibility).

If the aforementioned is not met, the token will not qualify as a security but as a financial instrument, hence the requirements of securities law are not applicable. For example, an issuer of a financial instrument which does not qualify as a security is not subject to prospectus obligations. However, the consequences are much more far-reaching because, for example, the criminal provisions under financial market law on insider trading and market manipulation only apply to securities.

Tokenization of investment fund units can revolutionize the way investors access and trade assets. The benefits of tokenization are numerous, for investors, issuers and investment fund managers alike and include the following:

Blockchain technology removes the need for (financial) intermediaries by providing a decentralized and transparent ledger for transferring, verifying, and clearing of transactions. This automatically results in more efficient transactions as transactions are settled and cleared within seconds. Furthermore, blockchain technology allows a high level of automation through smart contracts, which may execute transactions automatically based on predefined conditions. The transfer of fund units, including the settlement and clearing, can thereby be conducted instantly and at the same time. In addition, customized features can be programmed directly into the units (i.e. whitelisting, freeze, unfreeze, destroy and recreate, corporate actions, ban of specific countries etc.).

As mentioned, intermediaries become obsolete in a blockchain ecosystem, or, where they are still necessary, usually get a new role (e.g., banks). Consequently, tokenization will result in cost savings for the issuance of financial instruments as well as other processes, including corporate actions, reconciliation, and trading on the secondary market. Likewise, the possibility for automation as well as transparency in keeping record may significantly reduce costs for issuers, investors, and investment fund managers alike. Automation further significantly reduces the risk of errors. Accordingly, the management of complex compliance requirements becomes significantly cheaper, especially because specific rules can be programmed directly into each token.

Tokenized investment units may significantly improve compliance or at least facilitate the compliance management of an investment fund provided the necessary infrastructure exists. For example, both the financial markets regulations as well as the CISA provide for a mandatory segmentation of investor categories – some investment fund units may therefore only be offered to professional, qualified, or institutional investors but not to retail investors. By tokenizing an investment fund unit, it is possible to code such compliance rules into the token or into the smart contract (depending on the chosen blockchain protocol), i.e., by labeling the token as a unit meant only for professional investors. As a result, and in conjunction with a whitelist or blacklist (e.g. segmentation of investors into the above categories), such a token may only be traded by an investor who qualifies as a professional investor.

Similarly, other and individual compliance rules can be included in a tokenized investment fund units, such as trading halts or sanctioned individuals or countries. As blockchain and tokenization continue to gain traction, the adoption of this technology for compliance purposes is expected to offer transformative benefits across various industries and use cases.

The blockchain technology provides a distributed, immutable, and transparent ledger to record transactions and can thereby provide a single source of truth for all parties involved, improving transparency, and reducing disputes around record keeping. As a result, the utilization of blockchain technology is expected to result in enhanced efficiency and reliability in the trading, settlement and clearing of transactions. Blockchain technology further enables tracking and traceability of tokenized assets throughout their lifecycle, as each token representing an asset can be uniquely identified and recorded on the blockchain. This allows for transparent tracking of ownership, transfers, and other relevant information and provides a clear and auditable record of an asset’s history, assisting to prevent fraud, forgery, and other illicit activities.

Furthermore, tokenization of assets paves the way for asset management 2.0, as smart contracts can be programmed to invest according to a pre-programmed risk appetite and portfolio diversity, without the need for human interaction.

Tokenization can improve liquidity of investment fund units (and all other financial instruments) in two respects:

(i) Firstly, most investment funds are not listed and therefore tend to be illiquid. By issuing tokenized investment fund units, in theory, these units become immediately tradable on the blockchain making an illiquid product liquid as at least the possibility for a facilitated exchange of such investment fund units exists. In practice, however, and in particular to comply with the relevant laws, a respective trading venue is required.

(ii) Secondly, and this is mostly true for private equity fund units/instruments, traditionally, participating in a private fund or venture requires investing a considerable amount. Such large tickets can be daunting and require a substantial commitment, especially considering that the investment amount is usually subject to a lock-up period. Tokenization provides a remedy as a large ticket can be tokenized and be divided into several smaller tickets. The potential use cases are basically infinite and mostly depend on the fund structure (contractual vs. corporate fund structure or open vs. closed fund structure) as well as on the respective governing documents such as a (limited) partnership agreement or the fund agreement. These documents are ultimately also decisive for the question of who will tokenize the investment fund units or who will divide a large ticket into smaller ones. Theoretically, and as an example, the fund management may only issue tokenized fund units, or a large investor may tokenize and divide larger tickets into smaller ones.

Furthermore, tokenization also assists financial inclusion, as many people in developing countries do not have a bank account, let alone a trading account. However, almost everyone has a smart phone – including people in developing countries, provided there is stable and affordable internet connection. By tokenizing financial instruments, such instruments can also be made accessible in developing countries, since all that is needed to trade tokenized assets is a registered wallet on a smartphone and provided this is permissible by the applicable legal framework. Hence, more accessibility automatically leads to increased liquidity.

Tokenization has the potential to revolutionize the investment landscape by allowing for the creation of novel and innovative investment products, including fractionalized real estate, liquid revenue share agreements, dynamic ETFs, and other previously unmanageable offerings. This can expand investment opportunities for investors and generate new revenue streams for issuers, ushering in a new era of investment possibilities.

While tokenization offers numerous benefits, there are also challenges that need to be addressed. Challenges may include the following:

Tokenization presents unique and novel legal and regulatory complexities and requires, among other things, compliance with securities laws and regulations. The legal and regulatory frameworks surrounding tokenization in Switzerland are – in the international context – highly advanced and exemplary but still evolving, especially when it comes to their interpretation by the regulators. Consequently, it is necessary that issuers take measures to ensure compliance with all applicable laws and regulations.

Tokenization introduces novel technological hurdles, such as the imperative for robust cybersecurity protocols and the risk of technological disruptions that could impact asset trading and settlement/clearing processes. In addition, the increased use of blockchain technology may cause tokenization to face scalability issues, as networks may be limited in terms of transaction processing speed and capacity. Other issues may arise from the lack of interoperability or vulnerabilities due to coding errors or in the underlying blockchain technology itself. Therefore, in-dept knowledge and understanding of the underlying technology, its strategy as well as scalability solutions or other projects running on the blockchain are indispensable. Each project may or may not have a certain influence on the respective blockchain ecosystem as a whole.

The concept of tokenization still is relatively new, and it may take some time for it to be widely adopted. Issuers may need to educate investors on the advantages of tokenization and strive to establish trust in this technology. Furthermore, trading on the secondary markets still is a challenge today, as such exchanges hardly exist. Nevertheless, this challenge equally exists in the traditional financial system as pure liquidity is only certain if a market maker exists.

Tokenization presents a plethora of advantages for both issuers and investors, such as enhanced efficiency, cost reduction, improved compliance, heightened liquidity, increased transparency, and facilitated innovation. Nevertheless, there are also obstacles that must be tackled, including legal and regulatory issues, technological complexities, and market adoption challenges. As the legal and regulatory frameworks for tokenization evolve, issuers and investors can anticipate growing opportunities for investment and expansion in this promising emerging field.

When tokenizing real assets, the jurisdiction must always be taken into account, as various jurisdictions have different approaches and regulatory regimes – some are more favorable towards tokenization than others. It is advisable to contact a law firm with a corresponding track record before launching a tokenization project in order to avoid unwanted proceedings or penalties from regulatory authorities.

For more information on tokenization of private equity funds in Switzerland by example of the Limited Qualified Investor Fund: click here.

[1] The BCP-Framework has not been approved as such by FINMA